The Commonwealth Bank of Australia and Westpac have moved to temporarily scrap lucrative merchant service fees for electronic card payments in an attempt to stop more businesses shutting their doors, paving the way for a major rethink around how payments are clipped by institutions.

It was announced by CBA chief executive Matt Comyn and the head of Westpac’s business bank, Guil Lima – the bank is yet to appoint a new chief executive – in separate statements on COVID relief packages to flow from today as the government continues to discourage cash payments.

The hardcore steering of consumers away from cash and towards contactless or ‘tap’ payments by the government had been looming as a potential public relations disaster for banks because the sudden shift out of cash coupled with panic buying at supermarkets risked delivering a fee windfall at the direct expense of merchants.

According to Comyn, around 70,000 small businesses will have their merchant fees automatically waived.

Notably, CBA is also handing out terminal rental fee waivers to larger businesses that ask for them, a move that will bring some relief to retailers that have been forced into high street hibernation.

“Over the last fortnight we announced a number of measures to support our small business and retail customers through this very challenging period,” Comyn said.

“It has become apparent over the last week that medium-sized and larger businesses will also need significant support.”

Westpac says it is “refunding the merchant terminal rental fee for up to three months” with businesses told to either contact their relationship manager or apply online.

The announcement of the fee waivers came on the same day as the Australian Banking Association announced a cross-industry credit relief package made possible by the Australian Consumer and Competition Commission lifting regular controls on banks collaborating.

What’s less clear however is whether multinational payments giants Mastercard and Visa will also pass on fee relief or just leave it to the banks, who issue their cards and then collect hefty interchange fees through a convoluted series of merchant classifications and card type.

Visa and Mastercard have doggedly defended the operation of the interchange fee system that, like buy-now pay-later, extracts income from merchants by charging them to accept card payments, either physically or online.

At the same time merchants are also forced to pick up the bulk of the losses for online card fraud, even thought the banks and multinational payments schemes often own the networks and systems that are exploited.

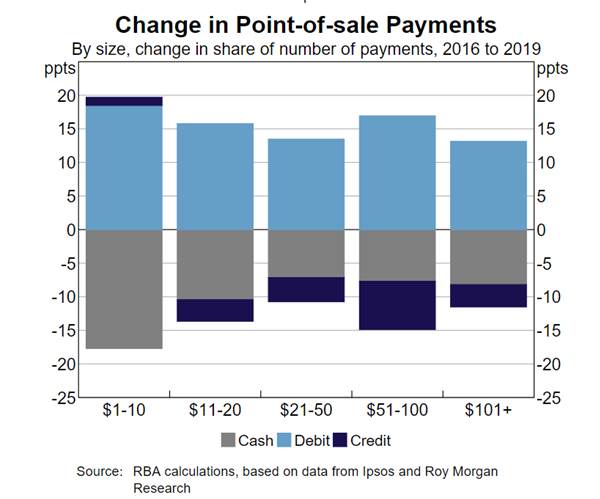

The other time bomb sitting in the mix of COVID-19 relief measures is the rapid rise of debit payments and their displacement of credit cards in the market.

According to the Reserve Bank of Australia’s latest study of consumer payments made using debit rocketed from 30 percent to 44 percent in terms of the share of the number of payments made below $9,999 between 2016 and 2019.

The graph below also illustrates the shifting mix.

The same study put credit cards falling from 22 percent to 19 percent across the same period, with cash dropping from 37 percent to 27 percent.

The problem for merchants, and now banks, is that because of the incentive structures put in place when contactless payments were first rolled out, most tap payments now route by default across Mastercard and Visa’s premium rails rather than across the cheaper eftpos network.

The tap-and-go hegemony of the two global card schemes has caused serious concerns at the RBA for years, especially its propensity to increase the cost of accepting card and online payments by merchants.

To address the issue, the RBA introduced reforms known as ‘least cost routing’ or ‘merchant choice routing’ where businesses got to choose what rails their payments rode on and thus could control the fee clip better – providing their bank actually offered them the choice, which they were meant to do.

The sluggishness of some banks to roll out and promote this drew uncharacteristically direct criticism from RBA governor Philip Lowe in December, statements that came as the RBA went to the now-postponed consultation on the review payments system, including stronger mandates for least cost routing.

With the review now postponed, cash on the nose and consumers being told to tap as the default, there’s now a serious question as to whether a more swiftly implemented mandate to bring medium term relief to merchants beyond the 90-day electronic payment fee holiday isn’t now a realistic option.

.jpg&h=140&w=231&c=1&s=0)

.png&w=100&c=1&s=0)

SAP NOW AI Tour ANZ

SAP NOW AI Tour ANZ

Forrester's AI Forum Sydney

Forrester's AI Forum Sydney

The 2026 iAwards

The 2026 iAwards

.jpg&w=120&c=1&s=0) Integrate 2026

Integrate 2026

Security Exhibition & Conference

Security Exhibition & Conference

_(1).jpg&h=140&w=231&c=1&s=0)